Key Takeaways

- Fintech apps without real-time fraud scoring at the API boundary face their first fraud incident within two post-launch weeks.

- Passing tenant ID as a controller parameter rather than enforcing it in the query layer creates exploitable data leakage bugs.

- Delegating card storage to a payment processor’s vault from day one is the highest-leverage security decision in a fintech build.

Fintech app development is among the strongest new business opportunities in 2026, but product teams consistently launch with two critical architecture gaps: missing fraud scoring and flat multi-tenant data isolation. San Diego fintech teams that skip these decisions spend their first post-launch sprint rebuilding them reactively, under live transaction pressure.

Fraud Detection and Tenant Data Isolation: How API Architecture Solves Both at Launch

The fix for both gaps sits at the API design layer, not in post-launch observability tooling. A real-time fraud scoring layer intercepts every transaction request before committing it, evaluating velocity, device fingerprint, and behavioral deviation within the same request cycle. Multi-tenant data isolation is enforced by binding the tenant context in the ORM query scope rather than passing tenant_id as a controller parameter that any service or background job can bypass.

Building the fraud detection layer before launch starts with a rule-based scoring engine checking three signals: transaction velocity per user account, geographic deviation from the user’s historical patterns, and transaction amount deviation from the user’s baseline. This layer runs synchronously at the API transaction boundary, blocks or flags the request before the transaction commits, and generates labeled signals for a machine learning layer added in a later sprint. According to the FFIEC IT Examination Handbook, transaction monitoring in financial applications should function as a real-time preventive control at the application layer, not as a batch audit process, which makes synchronous scoring the correct architectural baseline for any fintech API integration.

Flat tenant isolation, where tenant_id passes as a request parameter and gets filtered at the controller, creates a class of data-bleeding bugs that only surface when a second enterprise client onboards. Binding tenant context at the ORM query scope enforces the boundary at every database call, regardless of which controller, background job, or admin tool originates the query. Our team encounters this gap in roughly half of the fintech software development codebases reviewed at the architecture stage, and remediation scope grows sharply once the codebase crosses 20,000 lines.

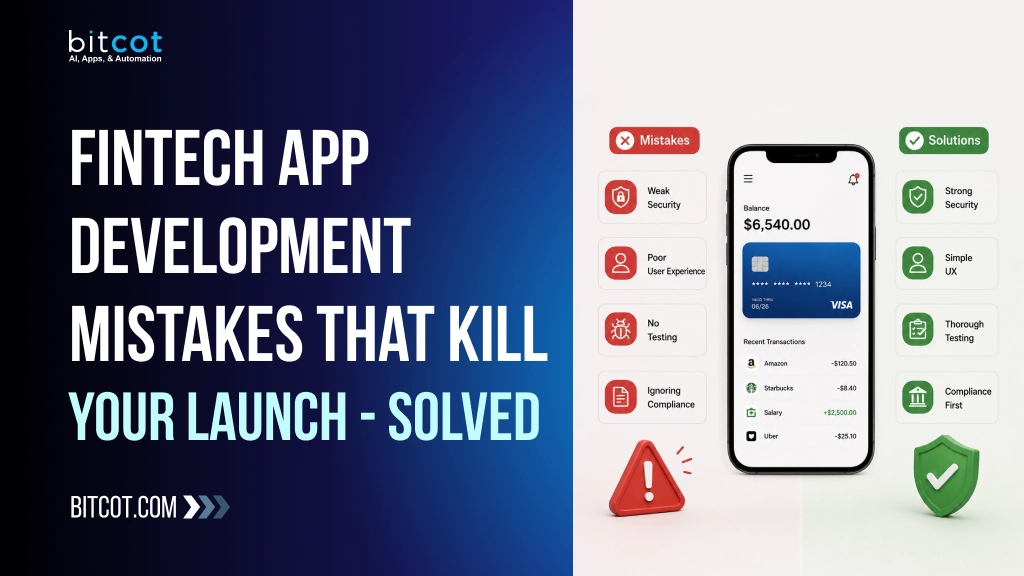

Exposed Payment Data and Gateway Failures: The Engineering Decisions That Prevent Both

The two most consequential engineering decisions in a secure payment app are where raw card data lives and how the application handles payment gateway failure. Delegating card data storage to the payment processor’s vault means your application layer never stores or processes raw card numbers, which reduces the security scope of everything downstream. Building a gateway orchestration layer as a first-class component means a single provider outage does not take down your checkout flow.

Teams that skip vault delegation and store card data in their own database carry a security footprint that extends to every service, log pipeline, and admin interface in their stack. The engineering decision to delegate storage to the processor’s vault from week one reduces that scope to the payment entry boundary. According to the Federal Reserve’s 2023 Payments Study, real-time and ACH payment volumes processed through third-party gateway infrastructure have grown consistently year over year, making gateway reliability a direct product availability dependency rather than an edge case a team can deprioritize at launch.

Payment gateway redundancy is engineered as an orchestration layer that routes transactions to a primary provider, detects elevated error rates above a configured threshold, and switches to a secondary provider within a single retry cycle. Teams that wire a single payment provider directly into the checkout flow face several engineering sprints of refactoring to add a second provider, which is why the abstraction layer is a launch decision rather than a post-launch enhancement. Teams building secure web app development infrastructure for financial products treat gateway orchestration as a required module in the initial architecture review, not an optional reliability upgrade.

What San Diego Fintech Builds Look Like Without These Two Architecture Decisions

In the fintech builds our San Diego engineers have reviewed, the pattern is consistent: teams that launch without fraud detection at the transaction boundary encounter their first fraud incident within the first post-launch weeks, then pause feature work to build the layer under live transaction pressure. Tenant isolation gaps appear later, typically when a second enterprise client’s data surfaces in a first client’s report during onboarding.

California founders who view fintech app development as one of the strongest new business ideas for 2026 should treat both of these decisions as launch criteria, not future backlog items. Our approach to custom software development in this space starts every fintech build with these two architectural contracts defined before the first feature is scoped.

Conclusion

The most expensive fintech app development mistakes are architecture decisions deferred from week one, not gaps in feature coverage. Before the first production transaction, confirm two things: your API enforces tenant isolation at the query scope rather than the controller layer, and your transaction boundary runs a fraud scoring check synchronously before committing. A team that locks both in before launch recovers from post-launch feature pressure without carrying the architectural debt that compounds across every sprint afterward.

Frequently Asked Questions

What is fintech app development?

Fintech app development is the process of building software applications that manage financial transactions, payment workflows, and financial data integrations with security and isolation architecture designed in from the start. It differs from standard web application development in that it requires explicit decisions about fraud detection at the transaction boundary, multi-tenant data scoping at the query layer, and payment data delegation to processor vaults before the first feature is written. Teams that treat fintech apps as standard web projects typically encounter expensive architecture corrections within the first post-launch quarter.

How does fintech API integration differ from standard REST API development?

Fintech API integration requires transaction-boundary fraud scoring, query-layer tenant enforcement, and tokenized payment routing that standard REST API patterns do not address by default. A standard API authenticates and routes requests; a fintech API must also enforce velocity anomaly detection, scoped tenant data access, and gateway fallback behavior at every transaction. The distinction is not syntactic — it is architectural: fintech APIs carry isolation and reliability contracts that general-purpose API design frameworks do not build in.

How does fraud detection work in a secure payment app?

Fraud detection in a secure payment app runs as a scoring layer at the API transaction boundary that evaluates the request before the payment commits. The layer checks velocity per user account, device fingerprint consistency, geographic deviation from the user’s historical baseline, and transaction amount anomalies. Teams that build this layer before launch tune thresholds against real transaction signals rather than building it reactively after encountering the first fraud event under live pressure.

What does fintech app development look like for teams in San Diego?

San Diego fintech development projects typically involve both enterprise financial clients and early-stage digital payment products, creating builds that must scale from controlled pilot environments to high transaction volumes without architectural rework. Our team in San Diego has observed that tenant isolation and fraud detection decisions made at project kickoff determine how cleanly that scale-up runs. California’s financial product market also introduces state-level data residency and consumer protection considerations that shape API design choices from the first architecture review.

Is custom fintech app development worth it compared to using a white-label payment platform?

Custom fintech app development is worth the investment when your product requires proprietary transaction logic, multi-tenant client management, or embedded financial workflows that white-label platforms cannot support. White-label payment platforms handle payment acceptance; they do not handle custom fraud rules, multi-provider gateway orchestration, or tenant-scoped financial data APIs. The engineering investment is justified by the product differentiation it enables and the architectural control it preserves as the product scales.