Key Takeaways

- The US healthcare AI market was valued at $8.65 billion in 2025 and is on track to hit $43.30 billion by 2030 (CAGR 38.0%).

- AI-enabled startups captured 62% of all US digital health VC funding in H1 2025, raising an average of $34.4M per round, an 83% premium over non-AI companies.

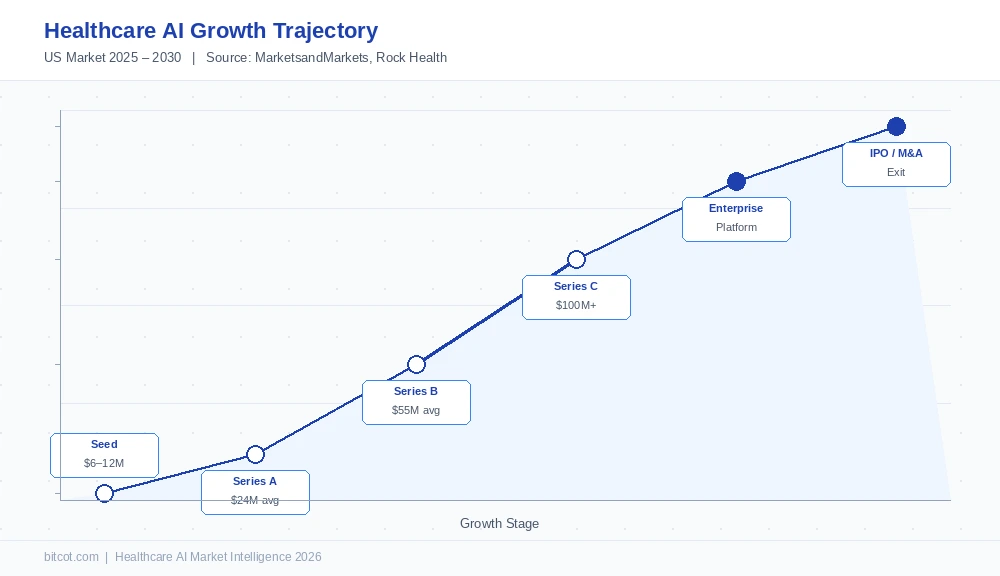

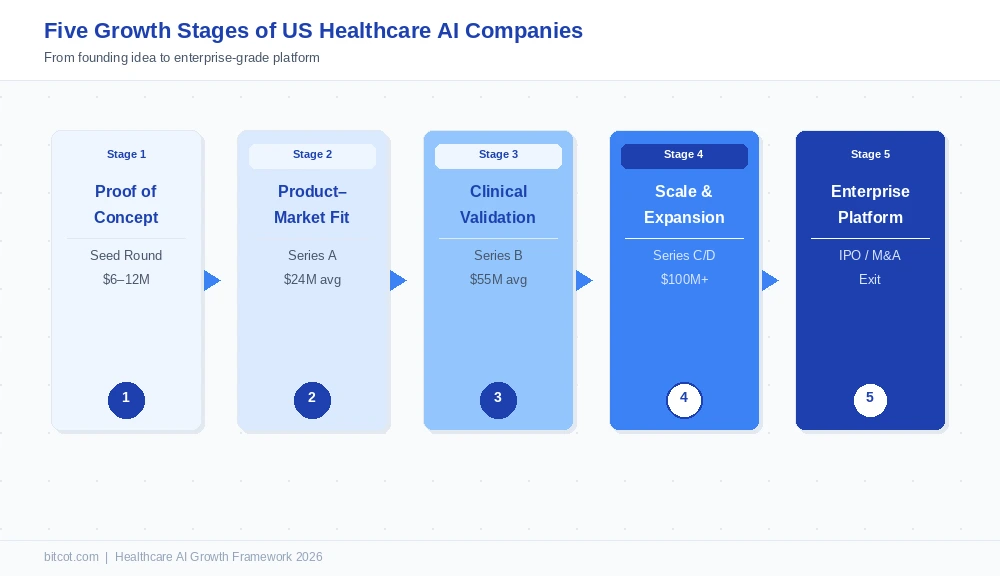

- Growth follows a clear arc: Seed → Series A → Series B/C → Enterprise platform → IPO or strategic M&A.

- Regulatory milestones (FDA SaMD clearance + data security standards) are not optional; they are the gatekeepers to enterprise contracts.

- The most successful firms begin with a single high-value wedge (e.g., ambient scribing, medical imaging AI) and expand horizontally into adjacent workflows.

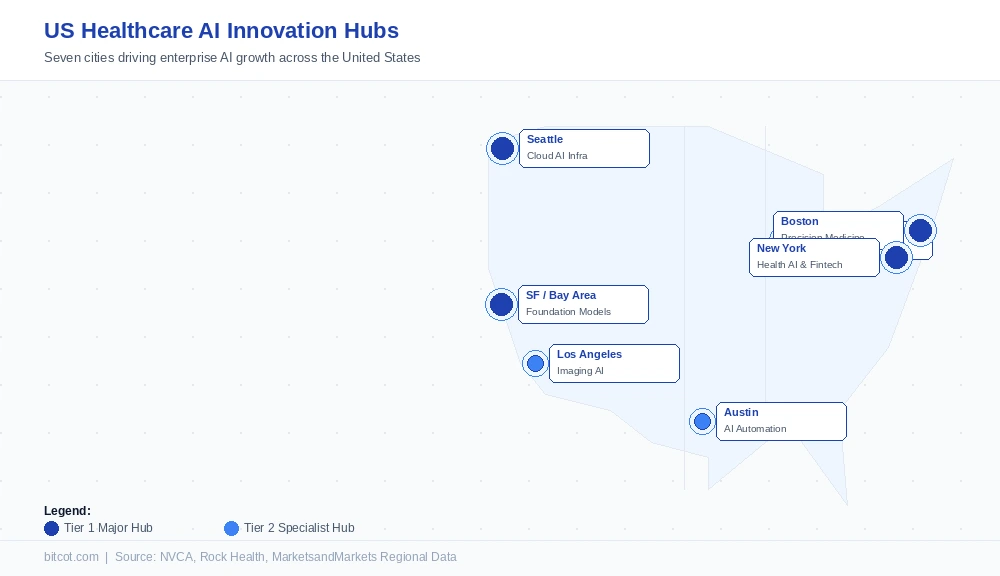

- Seven distinct US cities serve as the country’s leading healthcare AI hubs, each with a specialized ecosystem focus.

Introduction

A healthcare AI company does not simply wake up as an enterprise platform. The journey from a two-person founding team with a sharp clinical insight to a fully FDA-cleared, multi-hospital system vendor is one of the most demanding scaling paths in any industry. Yet thousands of companies are attempting it right now, and a growing number are succeeding at extraordinary speed.

In this guide, we break down exactly how healthcare AI firms grow in the US market: the funding stages that fuel each phase, the regulatory milestones that unlock enterprise sales, the regional clusters that offer the greatest competitive advantage, and the growth strategies separating the companies that reach enterprise scale from those that plateau at Series A.

The US Healthcare AI Market: Why Now Is Different

The healthcare AI investment wave of 2021 was speculative. The one happening now is structural. Providers, payers, pharma companies, and regulators have aligned in a way that makes AI adoption not just desirable but operationally necessary.

MarketsandMarkets data shows the US market advancing from $5.98 billion in 2024 to $8.65 billion in 2025, on a trajectory toward $43.30 billion by 2030 at a 38.0% CAGR. What is driving urgency among buyers is not just the technology but a convergence of workforce pressure, margin erosion, and proven ROI evidence that was largely absent before 2023.

Perhaps the most telling signal of market maturity is how deals are changing. According to Rock Health’s H1 2025 analysis, the number of deals has fallen slightly while average deal size has risen to $26.1 million, a sign that capital is concentrating in later-stage companies that have already demonstrated product-market fit. Early exploration is over; enterprise deployment is beginning.

The Five Stages of Healthcare AI Company Growth in the US

Not every healthcare AI startup follows an identical path, but the most successful ones all pass through recognizable phases. Understanding these stages is critical for founders planning their roadmap and for enterprise buyers evaluating which vendors have the organizational maturity to become long-term partners.

Stage 1 Seed

Proof of Concept: Identifying the High-Value Clinical Problem

Most healthcare AI companies that succeed begin not by asking, “What can AI do?” but “What does a physician, administrator, or patient need that currently takes far too long, costs too much, or produces too many errors?” The best seed-stage companies pick one well-defined problem, such as ambient clinical documentation, radiology read prioritization, or prior authorization automation, and build a tight, defensible solution around it. Seed rounds in healthcare AI averaged $6–12 million in 2025, typically involving one or two pilot health system partners who provide both funding signals and real-world data access.

Stage 2 Series A

Product–Market Fit: Proving the Wedge at Scale

Series A in healthcare AI, averaging $24 million per round in H1 2025, up 56% year-over-year per Rock Health data, is the stage where companies prove their wedge works across more than one or two pilot sites. The key investor question is: Does adoption accelerate without proportionally more sales effort? Companies that move from 2 hospital pilots to 20 without a 10× growth in sales headcount have found product-market fit. Those who cannot often never reach Series B.

Stage 3 Series B

Clinical Validation: The Regulatory Bridge to Enterprise

Series B is where healthcare AI companies must cross the regulatory moat that separates consumer-grade tools from clinical infrastructure. For any company whose AI directly informs a clinical decision, FDA clearance under the Software as a Medical Device (SaMD) framework is the price of admission to enterprise procurement. There are now over 340 FDA-cleared AI tools active in US clinical settings, covering everything from ECG analysis to lung nodule detection, and health systems increasingly require this clearance before signing multi-year contracts. SOC 2 Type II certification and robust patient data security architecture are parallel requirements at this stage.

Stage 4 Series C/D

Scale and Compliance: Expanding Horizontally into Adjacent Workflows

Menlo Ventures’ 2025 healthcare AI report makes a key observation: the most successful AI-native companies start with a single workflow and then expand into adjacent modules, steadily disintermediating legacy systems while building distribution moats. At Series C, a company that began with ambient scribing might add clinical documentation quality review, then billing code suggestion, then prior authorization automation. Each module deepens EHR integration, increases switching costs, and raises average contract value, the three pillars of enterprise stickiness. Average Series B and C rounds for AI-enabled health startups reached $55 million and above in H1 2025.

Stage 5 Enterprise / IPO

Enterprise Platform: Becoming Infrastructure

The final growth phase is when an AI company stops being a point solution and becomes foundational infrastructure, the intelligence layer through which an entire health system’s clinical and administrative workflows flow. Two exit paths dominate: IPO (Hinge Health and Omada Health both went public in H1 2025 after years of private growth, signaling that the public markets have re-opened for proven digital health platforms) and strategic M&A (private equity firms like New Mountain Capital are combining AI-native startups with legacy healthcare players to capture both technology and distribution in a single vehicle, a strategy that produced Smarter Technologies in May 2025).

US Regional Healthcare AI Hubs: Where Growth Is Happening

Geography matters more in healthcare AI than in most software categories. Clinical data partnerships, academic research pipelines, proximity to major health systems, and local regulatory expertise all cluster in specific cities. Understanding which hub aligns with your target vertical can significantly accelerate both product development and enterprise sales cycles.

San Francisco / Bay Area

Home to OpenAI, Anthropic, and Scale AI, the Bay Area accounted for over 35% of US AI venture funding in 2024. Healthcare applications built on large language models and multimodal foundation models are particularly concentrated here. Firms developing clinical reasoning assistants, genomic AI, and drug discovery platforms tap into an unmatched talent pool and a dense network of AI-specialized investors.

Boston

MIT and Harvard’s proximity has made Boston the dominant hub for research-backed healthcare AI, particularly in oncology, genomics, and precision diagnostics. Companies like Tempus AI and Insitro developed their scientific foundations in this ecosystem. Boston excels at translating academic research into clinical-grade AI products, with the PhRMA manufacturing corridor providing natural enterprise customer pipelines.

New York City

NYC drew more than $4.2 billion in AI startup funding in 2024, with a significant share going to companies at the intersection of financial services and healthcare revenue cycle management AI, claims adjudication automation, value-based care analytics, and payer-side fraud detection. New York’s dense concentration of major health systems (NYP, Mount Sinai, and NYU Langone) provides built-in enterprise customer access for Series B+ companies.

Seattle

Microsoft (Azure Health AI, Nuance DAX) and Amazon (AWS HealthLake, Amazon Comprehend Medical) have made Seattle the backbone provider for healthcare AI cloud infrastructure across the country. Companies building on these platforms benefit from direct access to health-specific AI APIs, secure cloud environments, and integrations with Epic and Cerner that are maintained by the platform providers themselves.

Chicago

Chicago’s strength lies in predictive analytics for large health systems and payers. The city’s proximity to some of the country’s largest integrated delivery networks, Northwestern Medicine, Rush, and Advocate Health, makes it a natural testing ground for AI-driven population health management, supply chain optimization, and predictive staffing systems. Chicago is increasingly where enterprise AI pilots become enterprise contracts.

Austin

Texas is now the second-largest state for AI job growth, and Austin’s growing startup base focuses heavily on AI-driven workflow automation for healthcare operations, patient scheduling optimization, prior authorization acceleration, and supply chain logistics. Lower operating costs and a business-friendly regulatory environment make Austin increasingly attractive for healthcare AI companies seeking to scale sales and implementation teams cost-efficiently.

Regulatory Strategy: The Non-Negotiable Growth Lever

Many healthcare AI startups treat regulatory compliance as a milestone to reach eventually. The companies that scale fastest treat it as a competitive advantage to build deliberately. Understanding the US regulatory landscape for AI in healthcare is not a legal exercise; it is a growth strategy.

Patient Data Security: The Baseline

Every company handling protected health information must maintain enterprise-grade data security from Day 1, aligned with HIPAA’s administrative, physical, and technical safeguard requirements. This means implementing appropriate administrative, physical, and technical safeguards for all patient data pipelines; executing Business Associate Agreements (BAAs) with every vendor who touches patient data, and maintaining audit logs that satisfy federal and state-level requirements. Health system procurement teams check data security posture before they check product features; failing this screen disqualifies a vendor before any clinical evaluation begins.

FDA SaMD Clearance: The Enterprise Gate

For any AI tool that supports, informs, or automates a clinical decision, the FDA’s Software as a Medical Device (SaMD) framework applies. The FDA has cleared over 340 AI and machine learning-based medical devices as of 2025, with the majority focused on radiology, cardiology, and pathology image analysis. Clearance timelines vary. A de novo authorization or 510(k) submission can take 6–18 months, but the companies that begin the process at Series A rather than waiting for Series B are materially ahead by the time enterprise procurement conversations begin.

The SOC 2 Type II Advantage

While not legally required, SOC 2 Type II certification has become a de facto requirement for enterprise IT procurement in healthcare. It signals that the vendor’s security controls have been independently audited over a sustained operating period, typically 6–12 months. For a healthcare AI startup, completing SOC 2 Type II before approaching health systems removes a significant procurement friction point and shortens sales cycles that are otherwise measured in years.

Five Proven Growth Strategies for Healthcare AI Firms

1. Start with the administrative layer, then move to Clinical

Administrative AI is the fastest-growing category because the ROI is immediate, measurable, and does not require FDA clearance. Ambient scribing tools generated $600 million in revenue in 2025, a 2.4× year-over-year increase, because every physician can see the time they save, and every CFO can measure the reduction in overtime hours for documentation staff. Companies like Abridge ($550 million raised in two H1 2025 mega-rounds) built deep clinical trust through administrative value before expanding into more complex clinical AI layers.

2. Embed Before You Expand

The most durable healthcare AI businesses are not standalone tools; they are embedded within existing EHR workflows. Epic’s App Orchard, Oracle Health’s ecosystem, and athenahealth’s Marketplace all provide distribution channels that bypass the cold outreach sales cycle entirely. Companies that invest in deep EHR integration early, even when it is technically complex, build switching costs that protect revenue and create upsell opportunities at contract renewal.

3. Publish Clinical Validation Evidence

Health systems and large payers are not consumer SaaS buyers. They require peer-reviewed evidence, outcome studies, and real-world data before committing to enterprise contracts. Healthcare AI companies that invest in publishing clinical validation studies, whether in journals like Nature Medicine, NEJM Evidence, or JAMA, create a durable sales asset that outperforms any white paper or case study. Peer review is the healthcare enterprise’s equivalent of a G2 review.

4. Pursue Strategic Health System Partnerships Early

A partnership with a major academic medical center, the Cleveland Clinic, Mayo Clinic, and Johns Hopkins, serves multiple simultaneous functions: it provides access to rich, labeled clinical data for model training; it generates the real-world evidence needed for FDA submissions; and it signals clinical credibility to subsequent enterprise buyers in a way that no marketing campaign can replicate. Companies like PathAI built their data moat through their Cleveland Clinic partnership, creating the foundation for international expansion.

5. Leverage the PE Roll-Up Opportunity

A new enterprise growth path has emerged in 2025: private equity-backed roll-ups combining AI-native startups with legacy healthcare services companies. New Mountain Capital’s creation of Smarter Technologies, merging Access Healthcare’s established distribution with the AI capabilities of SmarterDx and Thoughtful.ai, represents a playbook that bypasses years of organic sales growth. For AI companies with proven technology but limited enterprise distribution, a strategic PE partnership can accelerate market penetration by a factor of five or more.

Startup vs. Enterprise Healthcare AI: Key Differences

| Dimension | Startup Stage (Seed–Series A) | Enterprise Stage (Series C+) |

|---|---|---|

| Primary AI Use Case | Single high-value workflow (e.g., ambient scribing, imaging triage) | Multi-module platform across clinical, administrative, and operational workflows |

| Data Architecture | Partner data from 1–5 health systems, often structured as research agreements | Proprietary longitudinal dataset from 50+ health systems, with continuous retraining pipelines |

| Regulatory Status | Patient data security in place; FDA clearance in progress or not yet initiated | FDA-cleared SaMD, SOC 2 Type II certified, state-level privacy law coverage (CCPA, etc.) |

| Sales Cycle | 6–18 months; driven by clinical champion relationships | 12–36 months; driven by procurement committees, IT security review, legal, and C-suite sponsorship |

| Average Contract Value | $50K–$500K annually (pilot or departmental) | $1M–$10M+ annually (enterprise-wide or multi-year platform agreement) |

| Integration Depth | API or FHIR-based integration with 1–2 EHR platforms | Native EHR integrations, HL7 FHIR R4, SMART on FHIR, and bidirectional Epic/Oracle Health certification |

| Primary Growth Driver | Product excellence and clinical champion advocacy | Procurement committee approval, enterprise IT compatibility, and published outcomes evidence |

Real Challenges Healthcare AI Firms Must Overcome

The market opportunity is enormous, but the obstacles are proportionally significant. Understanding where healthcare AI companies most commonly stall and how leading firms navigate these challenges is essential for both founders and enterprise evaluators.

Legacy EHR Integration Costs

Epic and Oracle Health collectively serve more than 70% of US hospital beds. But integration with these systems is neither fast nor cheap. Smaller healthcare AI vendors frequently spend 30–40% of their engineering bandwidth maintaining EHR integrations that change with every platform version update. The companies that survive this challenge either build a dedicated integration engineering team early, partner with established middleware providers like Redox or Rhapsody, or join Epic’s App Orchard program and let Epic manage the integration surface.

The “Valley of Death” Between Series A and B

Bessemer Venture Partners’ healthcare data shows that the rate at which seed-funded companies progress to Series A within three years has significantly declined for recent cohorts, and the gap between Series A and B is particularly treacherous. Many companies run out of runway while trying to generate the clinical outcomes data that enterprise buyers require before committing to procurement. The companies that navigate this successfully typically secure a “lighthouse” health system partner, one prestigious enough that their contract acts as social proof for all subsequent buyers, and then race to publish outcomes data from that relationship.

Physician Adoption Friction

The best AI in the world fails if clinicians reject it. Physician adoption in healthcare AI is directly tied to workflow friction: tools that require physicians to change how they document, where they click, or how they interpret results face adoption resistance that can kill a company even after a successful enterprise sale. Companies leading in physician adoption, Abridge, Suki, Nabla, share a common design principle: AI should make the physician’s existing workflow easier, not teach them a new one.

Data Privacy and Algorithmic Bias Risk

Healthcare AI models trained on non-representative datasets can produce systematically biased outputs that harm underserved populations, a risk that regulators, health systems, and investors are increasingly scrutinizing. Companies that proactively audit their training data for demographic representation, publish bias evaluation results alongside clinical validation studies, and implement ongoing bias monitoring in production deployments are substantially better positioned in enterprise procurement than those that treat this as a compliance checkbox.

Conclusion: The Enterprise Window Is Open, But Not Indefinitely

The US healthcare AI market has moved past experimentation. Health systems are no longer asking whether AI belongs in clinical workflows; they are asking which vendors are mature enough to trust with enterprise-wide deployments. That question creates the greatest opportunity in a generation for companies that have done the work: built clinical validation, secured regulatory clearances, and embedded deeply in EHR workflows.

For early-stage companies, the roadmap is clear: pick one high-value problem, prove it at scale, and treat every pilot as an opportunity to build the evidence that makes the next contract inevitable. For health systems evaluating vendors, concentrate spending on architectures that scale from departmental to enterprise-wide without a rip-and-replace cycle.

That is exactly where Bitcot works. We help healthcare AI companies at every stage, from architecting a defensible MVP around a single clinical wedge to building EHR integrations that survive enterprise procurement scrutiny. We have delivered production-grade healthcare platforms across the US market and understand the technical complexity that separates pilots from contracts.

If you are building a healthcare AI product or scaling toward enterprise deployment, the next step is simple map your current architecture against what health systems actually require.

Talk to Bitcot’s healthcare AI team →

Frequently Asked Questions (FAQs)

How do healthcare AI startups grow into enterprise companies in the US?

Healthcare AI startups scale into enterprise companies by progressing through defined funding stages (Seed → Series A → Series B/C → IPO or M&A), securing FDA clearances for clinical tools, forming strategic partnerships with major health systems, and expanding from a single-use-case wedge into broader platform offerings. The fastest-growing companies start with high-ROI administrative automation and use that foundation to earn the clinical trust and data access needed for more complex AI deployments.

What is the US healthcare AI market size in 2025–2026?

The US healthcare AI market reached approximately $8.65 billion in 2025 and is projected to reach $43.30 billion by 2030, growing at a compound annual growth rate (CAGR) of 38.0%, according to MarketsandMarkets research. North America accounts for over 40–54% of the global market, depending on the source, making it the single largest regional market for healthcare AI investment and deployment.

Which US cities are the biggest hubs for healthcare AI companies?

The seven leading US healthcare AI hubs each specialize in different segments: San Francisco/Bay Area (foundation models and platform AI), Boston (precision medicine and biotech AI), New York City (health fintech and enterprise AI), Seattle (cloud infrastructure for health AI), Austin (workflow automation), Chicago (enterprise data analytics), and Los Angeles (imaging AI and digital health media). Choosing the right hub depends heavily on which vertical and buyer type a company is targeting.

What regulatory approval do healthcare AI companies need in the US?

US healthcare AI companies must implement enterprise-grade patient data security for all protected health information. Clinical AI tools that directly inform or automate medical decisions must also obtain FDA clearance as Software as a Medical Device (SaMD), typically via 510(k) submission or De Novo authorization. Enterprise procurement also commonly requires SOC 2 Type II certification and state privacy law compliance (CCPA for California, etc.). Over 340 FDA-cleared AI tools are now active in US clinical settings, primarily in radiology, cardiology, and pathology.

How much venture capital is flowing into healthcare AI?

In H1 2025, AI-enabled healthcare startups captured 62% of all US digital health venture capital, approximately $4 billion of the $6.4 billion raised. AI startups raised an average of $34.4 million per round, an 83% premium over non-AI companies. Nine of the 11 “mega deals” (over $100 million) in H1 2025 went to AI-enabled companies. For the full year 2025, firms with AI offerings collected 54% of all digital health funding, up from 37% in 2024, according to Rock Health’s annual report.

What is the biggest mistake healthcare AI companies make when trying to scale?

The most common scaling mistake is trying to expand the product footprint before achieving deep integration and high utilization within the initial use case. Enterprise health systems will not expand a vendor relationship regardless of the additional modules offered until the primary deployment demonstrates measurable, sustained clinical or operational value. Companies that rush to build a platform before proving their wedge consistently underperform those that go deep on one problem first, publish outcome data, and let demonstrated ROI open the door to adjacent modules.